The ability to map investor data across several jurisdictions efficiently is not a luxury but a necessity for fund managers operating on a global scale. Regulatory friction, therefore, has become a key performance metric within the investment management industry today as inefficient investor data mapping across jurisdictions limits capital velocity. However, many fund managers are still forced to deal with redundant compliance workflows as legacy systems treat compliance as a series of isolated checklists rather than a unified data management workflow. The most common culprit is the use of unstructured pdf documents and email communications for investor documentation collection and verification. For an investment firm to aggressively scale operations in 2026, a major pivot in this process is necessary. The goal should be to treat compliance as a data inheritance architecture, not a simple document collection task.

The Architecture of the Golden Record

The biggest regulatory hurdles are faced by LPs that invest across several jurisdictions. Such an LP might invest in four different vintages across three or four different jurisdictions. The legacy compliance architecture forces this LP to maintain separate accounts for each of these jurisdictions, each requiring its own siloed KYC documents, tax validation, and contact updates.

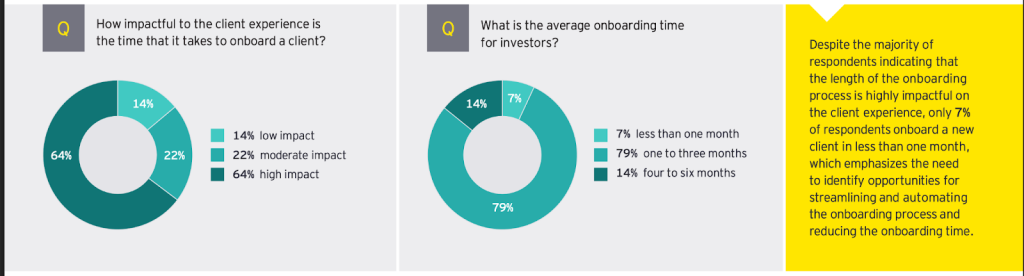

This friction has led to real-world constraints for LPs. For instance, according to a recent EY industry survey, 64% of fund managers acknowledge that lengthy onboarding severely impacts the investor experience, yet less than 7% are able to onboard institutional investors in under a month. Capgemini also found that nearly a third of investment firms take three months or longer to onboard sophisticated capital, which highlights the inefficiency of the client onboarding process despite investments in improving digital capabilities.

Exhibit 1: EY survey results on the client onboarding experience

Source: EY

When sophisticated investors are forced to resubmit trust deeds and utility bills they have already provided to the same firm, it signals operational immaturity. As evident by the above survey results, this regulatory friction can lead to lost capital for investment firms.

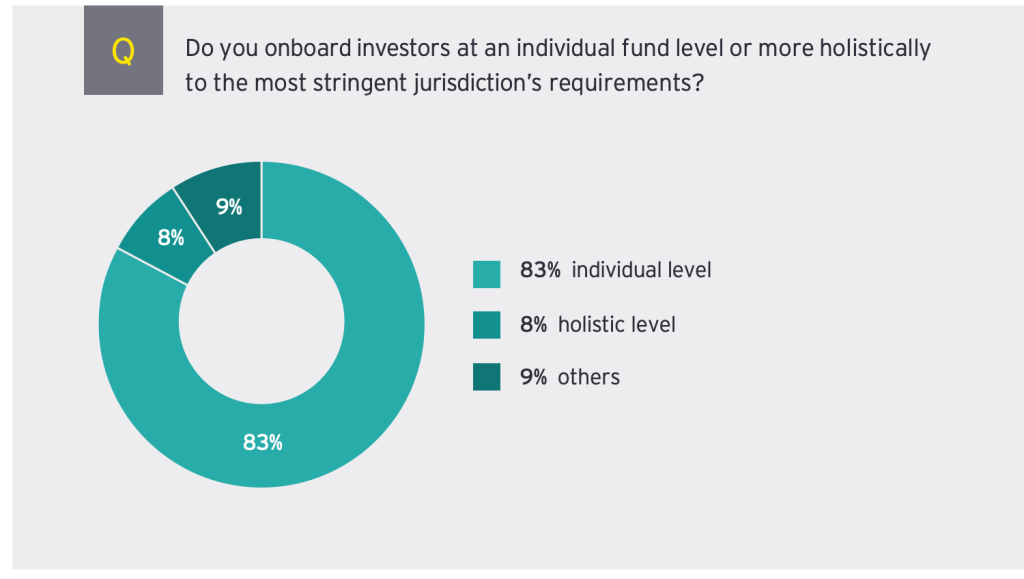

EY’s survey results further highlight how fund-level, manual KYC processes still dominate compliance workflows among investment firms. This is at the center of the inefficiencies seen within the investment industry.

Exhibit 2: Individual fund level KYC processes dominate compliance workflows

Source: EY

The solution lies in shifting to identity-centric architecture, often referred to as the golden record in the investment industry.

Technically, this requires an entity resolution layer. Instead of attaching compliance data to a specific fund, the data is attached to a unified digital identity which can be thought of as a master profile. When an LP uploads a document to this master profile, the system acts as a single source of truth. All downstream funds will have access to these documents seamlessly.

This entity resolution layer can boost the efficiency of the compliance workflow for an LP. For example, if an LP subscribes to a new fund in Luxembourg after setting up shop in the U.S.,, the system simply queries the golden record. It verifies that the identity is already compliant, flagging only the specific delta required for the new jurisdiction.

This architecture is the core logic behind RAISE Connect. By serving as the central ingestion point for investor data, it creates a digital identity that feeds directly into the back-office systems such as RAISE FAS and compliance engines such as RAISE CRA. The result is an onboarding workflow that respects the LP’s time and mitigates the risk of client churn.

Dynamic Rule Engines vs. Static Checklists

For decades, compliance workflows have relied on static checklists based on the specific jurisdiction where an LP resides. The primary vulnerability of such a hard-coded compliance workflow is the sheer velocity of global regulatory change. According to the benchmark Thomson Reuters Cost of Compliance Report, financial compliance teams must now navigate over 61,000 regulatory events annually, averaging more than 160 regulatory alerts per day. Given this high velocity of regulatory events, a static checklist is obsolete the moment it is deployed as updating such a system requires manual intervention.

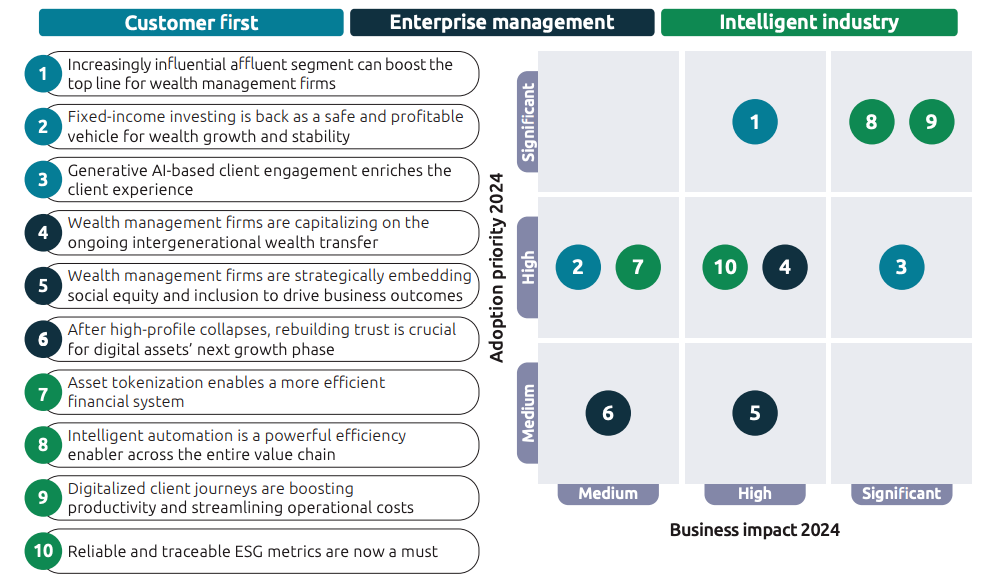

Exhibit 3: Intelligence automation is expected to be a major efficiency enabler

Source: Capgemini

The architectural fix is transitioning to a dynamic rule engine that abstracts regulatory logic away from the underlying LP data. Consider an LP investing simultaneously in a U.S. fund governed by SEC rules and a Luxembourg fund governed by AIFMD and GDPR. Instead of generating two separate onboarding packs, a dynamic engine evaluates the LP’s golden record against the specific jurisdiction tags of both funds. This system can then generate a single consolidated request for the missing documents.

This is the operational mechanism behind RAISE CRA, which functions as a dynamic engine rather than a static form builder.

Data Lineage and Standardized Audit Trails

Regulatory bodies like the SEC and Luxembourg’s CSSF are increasingly demanding regulatory data lineage. The idea behind these requests is to create an audit trail to verify the approval of compliance checks at the firm level. This has created a new challenge for investment firms that historically relied on snapshot reporting.

To scale efficiently amid this changing regulatory environment, investment firms need to transition from snapshot reporting to event-sourced logging. In an event-sourced system, every single change to an LP’s profile is recorded as an immutable event which makes it easier for the firm to reconstruct its compliance checks at any given time in the future.

Many investment firms have already begun transitioning to event-sourced systems. According to Gartner, by the end of this year, 20% of large enterprises will use a single data and analytics governance platform to unify and automate their data lineage.

API-First Compliance Architecture to Support Interoperability

A unified, smart compliance workflow is not just about improving the efficiency of the compliance process but about improving the overall efficiency of an LP. This is why such a system should trigger other operational workflows across the platform, including capital calls and tax reporting.

In the tech stack model used by investment firms historically, compliance data was manually transferred between systems. Given the many systems involved in cross-border operations, this manual intervention often leads to data friction and deployment delays.

This is where an API-first compliance architecture steps in. Such a system prioritizes interoperability. The RAISE ecosystem is built on this exact architectural logic. Once an LP is cleared through RAISE CRA, the API automatically grants them access to the RAISE Connect investor portal and feeds the verification status directly into RAISE FAS, the fund admin ledger.

Conclusion

Obsolete, inefficient compliance workflows can materially slow down an investment firm’s ambitious goals to scale across jurisdictions. The old tech stack model of relying on manual checklists and disconnected databases is no longer working. For modern investment firms, a well-designed compliance architecture is a scalable asset, not just a back-office cost center. By treating compliance as a data inheritance architecture, RAISE turns regulatory friction into a streamlined, automated workflow.

Book a demo to explore the RAISE ecosystem and get a technical deep-dive into how you can build a smarter compliance infrastructure today.