In public markets, risk is priced in real time. This enables investors to react in real time. In private markets, however, risk has historically been a lagging indicator. Relying on quarterly reporting cycles to manage multi-million-dollar capital deployments is a systemic flaw. Waiting 45 days after a quarter end to review a static PDF means GPs and LPs are constantly reacting to stale data.

This delayed reaction time is a massive liability in the current macroeconomic environment. According to Bain & Company, median holding periods for buyout funds have stretched to an average of seven years. This extension has created an industry-wide exit backlog of roughly 32,000 unsold companies worth $3.8 trillion. With holding periods extended and entry multiples remaining elevated, financial engineering can no longer be relied upon as the primary source of alpha.

Investment returns today must be driven by strict operational improvements and early risk mitigation rather than solely relying on multiple expansions. Operational execution and early risk identification are the only reliable ways to defend the illiquidity premium in private markets as well. Because of this, investment firms that lack advanced analytics capabilities to identify portfolio risk early are already starting behind the line.

Real-Time Data Aggregation vs. Static Reporting

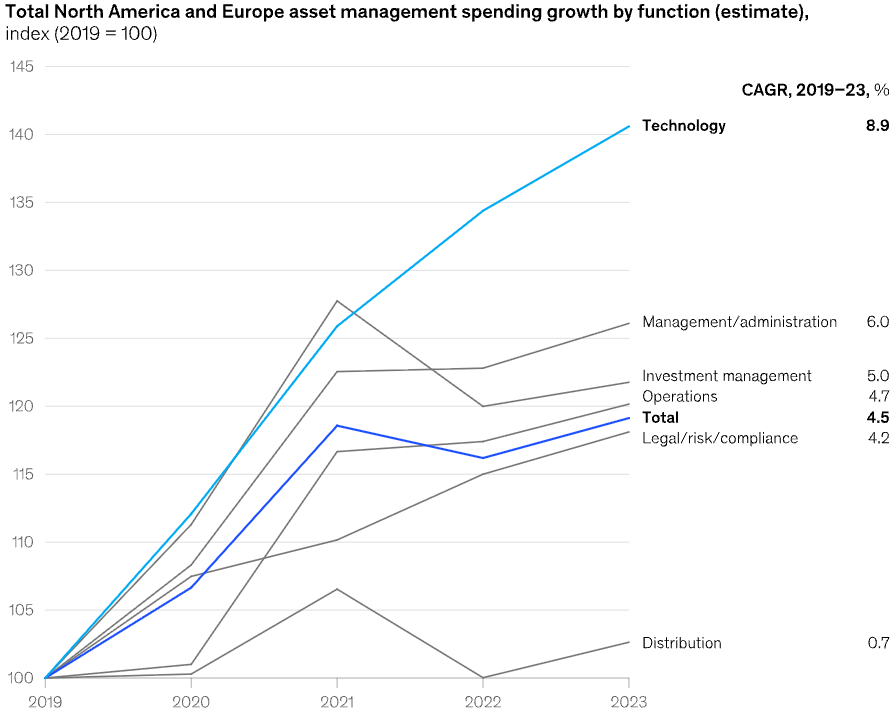

Legacy technology stacks rely on snapshot reporting where data is often reported with a lag rather than in real time. This approach creates severe operational friction. Not surprisingly, the gap between tech-enabled firms and legacy managers is widening rapidly. According to McKinsey, leading sponsors utilizing AI and advanced data analytics for portfolio monitoring report 30% to 40% productivity gains in analyst-intensive tasks. This is exactly why the asset management industry has doubled down on technology investments in the past few years.

Exhibit 1: Technology spending in the asset management industry

Source: McKinsey

The RAISE ecosystem steps in to close this exact gap. Many software providers attempt to solve the data silo problem by patching different systems together with clunky API integrations. RAISE takes a fundamentally different approach. The back-office fund administration tools within RAISE FAS and the front-office investor portal within RAISE Connect operate on the exact same platform. They do not need to connect through an API because they are the same product.

This native unification replaces static reporting with dynamic automated data feeds. The architecture natively supports real-time data aggregation. The moment a financial metric updates in the accounting ledger, it becomes immediately available for risk analysis. This eliminates data friction entirely and allows analysts to focus on predictive modeling rather than manual reconciliation.

Identifying Variance and Covenant Risk Before the Breach

Historically, within private markets, performance tracking has always been thought of as a sufficient risk management tool. This is no longer the case. Investment firms must transition to predictive analytical tools to limit the downside potential. Advanced portfolio analytics allow GPs to instantly flag deviations from target metrics before they trigger a catastrophic event.

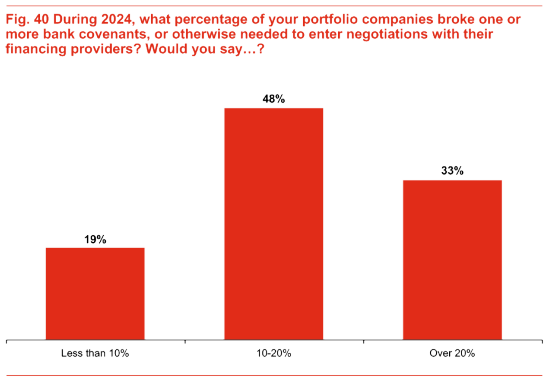

The consequences of missing these early warning signs are severe. According to PwC, 33% of private equity firms reported that more than 40% of their portfolio companies breached a debt covenant or required renegotiation with lenders in the past year. These breaches are rarely sudden. They are usually preceded by quarter-over-quarter margin compression that goes unnoticed in static Excel models.

Exhibit 2: Percentage of portfolio companies that broke one or more bank covenants in 2024

Source: PwC

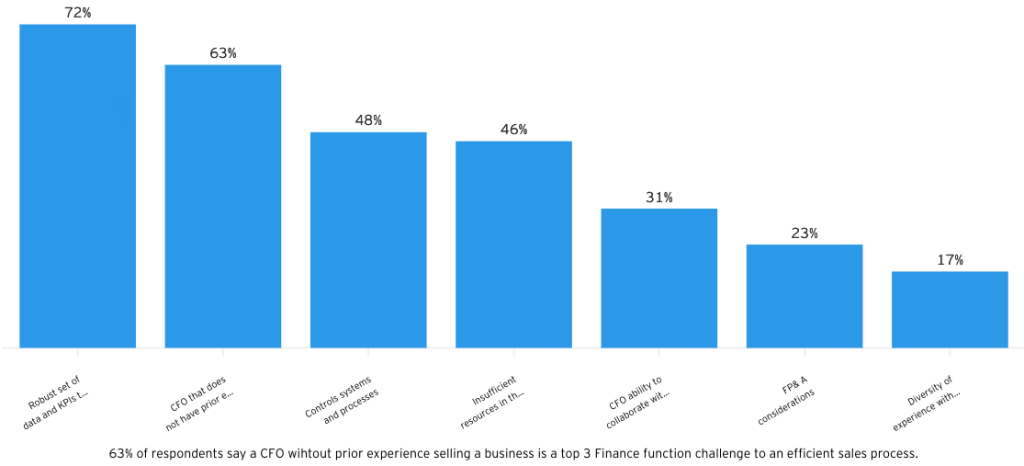

Simply identifying the risk is only half the battle as well. According to EY, 41% of PE firms report a severe lack of access to data granularity to properly support their equity story or defend their valuations. If a portfolio company’s EBITDA margin compresses by 200 basis points, the GP needs to know instantly rather than 45 days after the quarter closes.

Exhibit 3: Areas of the finance function that PE firms find most challenging to an efficient sales process

Source: EY

By leveraging automated variance analysis, investment platforms can immediately alert fund managers to these negative trends. This is where a system such as RAISE Portfolio Management that tracks the live data flowing from the accounting ledger and compares it against the underwriting model comes in handy. In addition to already available features, the system will have the capability to raise a flag automatically in the future if a debt covenant threshold approaches.

For a technical breakdown of how to track these critical metrics in real time, download the brochure for the RAISE Portfolio Management software.

Cash Flow Forecasting and the DPI Imperative

The current private equity landscape is facing a severe liquidity logjam. Because exit markets remain constrained, Distributions to Paid-In capital, or DPI, is now considered as the most critical performance metric for LPs. McKinsey confirms this structural shift in investor priorities in their latest Private Markets Annual Review. Managing illiquidity risk in this environment requires more than just historical reporting. It requires accurate and forward-looking cash flow forecasting.

When distributions stall, LPs suffer from the numerator effect. Their private equity allocations remain artificially high relative to their total portfolio. This forces them to scale back future investments. McKinsey analysis indicates that an overallocation of just 1% to private markets can reduce an LP’s planned commitments to new funds by up to 12% annually. This severe consequence highlights the urgent need for real-time cash flow and exposure forecasting.

To navigate this, investors must utilize dynamic rule engines to run scenario models on future cash flows. Advanced portfolio analytics platforms allow LPs to model capital call pacing against expected distributions under various macroeconomic stress tests. This proactive forecasting helps investors avoid the numerator trap and maintain their strategic allocation targets without risking a default on future capital calls.

Conclusion

In a market defined by extended hold periods and persistent macroeconomic stress, the old technology stack model is a severe liability. Relying on disconnected systems and lagging indicators exposes both GPs and LPs to unnecessary vulnerabilities. Advanced portfolio analytics fundamentally transitions risk management from a defensive compliance necessity into an offensive competitive advantage.

By adopting a natively unified data architecture, investment firms can eliminate operational friction and monitor risk in real time. The ability to forecast cash flows accurately and identify covenant breaches before they happen is what separates top quartile performers from the rest of the market. Investment firms that fail to upgrade their infrastructure will struggle to defend their valuations and risk losing their strategic allocations in the long run.

Book a demo to explore the RAISE ecosystem and get a technical deep dive into how you can build a smarter, globally scalable analytics infrastructure today.